finances.nw is NeuraWeb's economic transparency and financial empowerment platform — combining live economic data, government spending transparency, and full personal and business financial management. This is not a surface conversation. We sat down with S. Vincent Anthony (vincent.nw), founder and CEO of NeuraWeb Global Inc., and asked him to go deep — on the mechanics of financial extraction, on what's coming, and on why he believes a permanent verified identity is the most important financial tool the average person doesn't yet have.

NeuraWeb: Let's start with a concept most people have never heard of — the Cantillon Effect. What is it and why does it matter more than almost anything else in economics?

Vincent: The Cantillon Effect is the single most important economic mechanism that almost no one in mainstream media ever names — and that silence is not accidental.

Richard Cantillon was an Irish-French economist writing in the 1700s. He observed something that sounds simple but has profound implications: when new money enters an economy, it does not distribute evenly or simultaneously. It enters at a specific point — and the people closest to that entry point benefit enormously, while the people farthest from it are actually harmed.

Here's the modern version. The Federal Reserve creates money — through bond purchases, through reserve expansion, through the mechanisms of quantitative easing. That money goes first to the primary dealer banks. The banks use it to buy assets — equities, real estate, bonds. Asset prices rise. The people who already own assets see their net worth increase before a single dollar has reached wages, before a single price in a grocery store has adjusted.

Then the money filters outward. By the time it reaches the worker as a wage increase — if it reaches them at all — prices have already moved. The grocery store has already adjusted. The landlord has already raised the rent. The worker got the dollar after the purchasing power was already extracted from it.

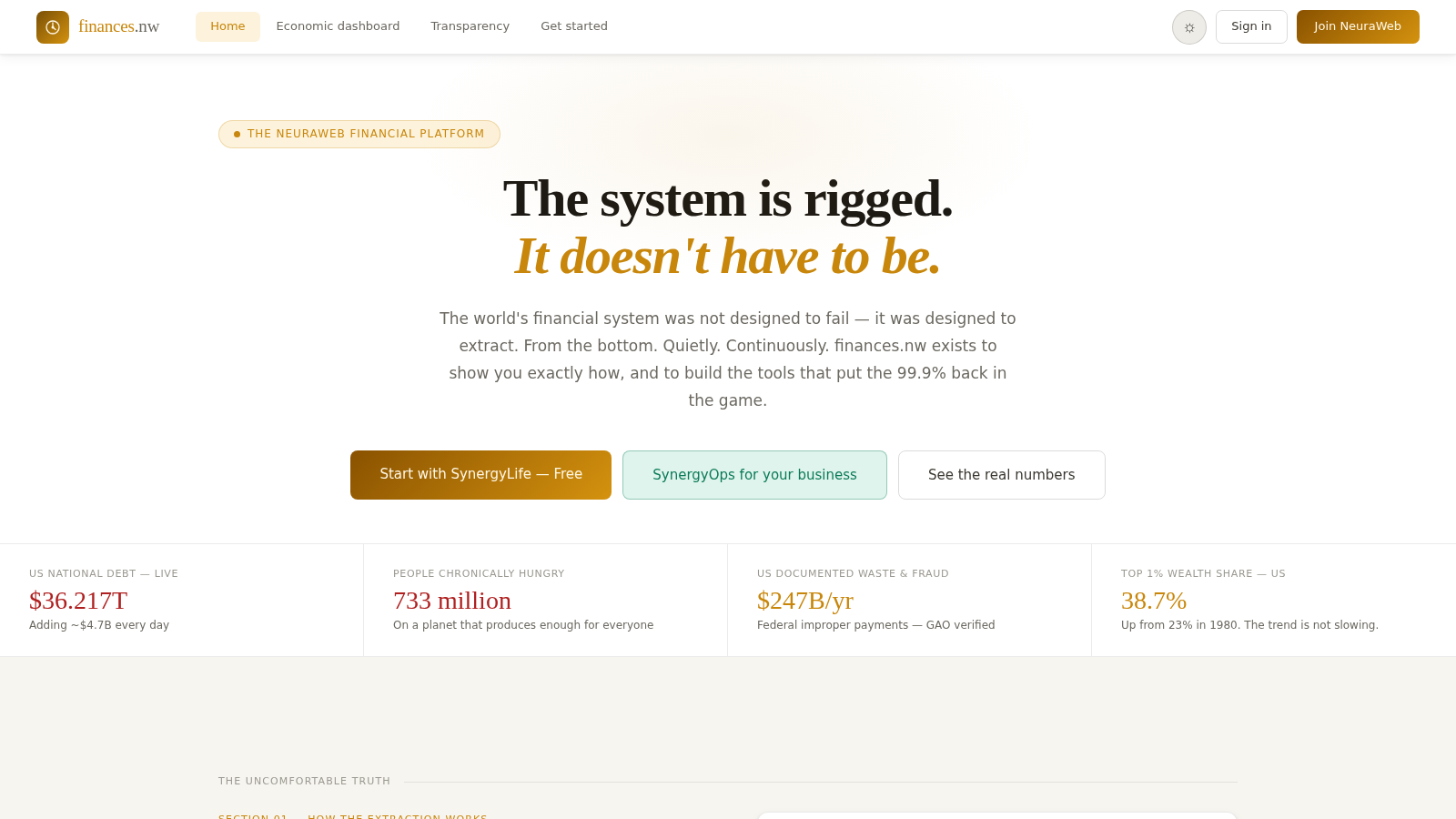

This is why every major round of money creation since 2008 has widened the wealth gap. It is not a bug. It is not an unintended consequence. It is the Cantillon Effect operating exactly as described three hundred years ago. The top 1% owned 23% of US wealth in 1980. They own 38.7% today. The quantitative easing programs of 2008, 2020, and the intervening years transferred trillions of dollars of real purchasing power from people who hold wages and cash to people who hold assets — legally, quietly, and with the full endorsement of the institutions designed to prevent exactly this outcome.

When I say the system is working as designed — this is what I mean. Not conspiracy. Arithmetic.

NeuraWeb: The petrodollar. Most people have heard the word. Almost nobody understands what it actually means or why its fracture matters to their daily life.

Vincent: The petrodollar is the reason the United States has been able to run a $36 trillion national debt without the kind of currency collapse that would have destroyed any other economy on earth decades ago. Understanding why requires going back to 1971 and 1974.

In 1971, Nixon closed the gold window. The dollar was no longer convertible to gold at a fixed rate. This should have been catastrophic — you've just told the world that your currency is backed by nothing tangible. What saved the dollar was a deal struck with Saudi Arabia in 1974. The United States guaranteed Saudi security and weapons sales. In exchange, Saudi Arabia — and eventually the entire OPEC bloc — agreed to price oil exclusively in US dollars and to recycle their surplus petrodollars into US Treasury bonds.

The consequence was structural and permanent: every nation on earth that needed oil — which is every nation on earth — needed dollars to buy it. This created an artificial, sustained global demand for the US dollar that had nothing to do with the underlying productivity of the American economy. It allowed the US to run deficits that would have been impossible for any other currency. It allowed Americans to consume more than they produced for decades. It exported inflation to the rest of the world rather than absorbing it domestically.

Now that architecture is fracturing. China and Russia settled oil trades in yuan in 2023. India bought Russian oil in rupees. Saudi Arabia opened discussions about accepting non-dollar payment for oil. The BRICS nations — Brazil, Russia, India, China, South Africa, and now Egypt, Ethiopia, Iran, and the UAE — have explicitly stated their intention to reduce dollar dependence in bilateral trade.

This is not a conspiracy theory. These are documented, public, geopolitical negotiations. The question is not whether petrodollar dominance will decline. It is how fast and what the consequences are.

For the average American, the consequence is this: the artificial global demand for dollars that allowed the US to consume beyond its means and export inflation for fifty years is diminishing. As it diminishes, the inflation that was exported comes home. The purchasing power that was subsidized by the rest of the world's need for dollars becomes unsubsidized. The math on $36 trillion of debt at 4.25% interest — $1.5 trillion in annual interest payments — becomes harder to sustain when the buyer base for Treasury bonds is contracting.

I am not predicting collapse. I am pointing at a structural shift that is already underway and that the people it will affect most have not been told about in plain language. That is exactly why finances.nw exists.

NeuraWeb: Financialization. The word gets used but rarely explained. You said housing stopped being shelter in 1980 and became an asset class. What happened and what does it mean for someone trying to buy a house today?

Vincent: Financialization is what happens when essential human needs — shelter, healthcare, education, food — get converted from things people use into assets that people invest in. And the conversion point is always the same: when financial capital discovers that a captive market exists, it moves in.

Housing is the clearest example. Before the 1980s, the primary buyer of a house was someone who intended to live in it. The price of housing was therefore anchored, imperfectly but meaningfully, to what a household could afford to pay out of income. When institutional capital entered the housing market at scale — when private equity firms began buying single-family homes in bulk, when real estate became a standard portfolio asset class, when mortgage-backed securities created a mechanism to financialize housing debt itself — the price anchor changed. Housing was no longer priced against what a family could afford. It was priced against what a return-seeking investor would pay.

The result is documented and measurable. US home prices have risen approximately 400% since 1984 in real terms. Median household income has risen approximately 20% in real terms over the same period. The gap between what housing costs and what wages support is not a supply problem — though supply is also constrained, often deliberately by the same investors who benefit from scarcity. It is a financialization problem. Capital competes with labor for housing, and capital always wins because capital is not constrained by income.

The same mechanism operates in healthcare. The United States spends approximately 17% of GDP on healthcare — nearly double what peer nations spend — and produces worse outcomes by almost every metric. Why? Because healthcare was financialized. Hospital systems became portfolio companies. Pharmaceutical companies became royalty streams. Insurance became a rent-extraction mechanism sitting between the patient and the physician. Every dollar that goes to administration, to investor return, to executive compensation at a for-profit hospital system, is a dollar that was extracted from a person who had no alternative but to pay it. Captive market. Financialization. Extraction.

Education followed the same path. The federal student loan program, created to expand access, became the mechanism by which university pricing was deanchored from any relationship to value. When the government guarantees loans regardless of the borrower's ability to repay or the quality of the credential, universities have no incentive to control costs. The result is $1.7 trillion in student loan debt, credential inflation that requires a degree for jobs that didn't require one a generation ago, and an entire generation that bought an asset — a degree — whose price was set by financialization, not by the labor market that was supposed to absorb them.

This is the pattern. Find a captive need. Financialize it. Extract rent from the captive. The people who cannot exit the market — who need shelter, who need healthcare, who need education, who need food — pay the extraction cost. The people who own the assets that provide these necessities collect it.

NeuraWeb: Central Bank Digital Currencies — CBDCs. Governments are framing them as modernization, as efficiency. What are they actually?

Vincent: CBDCs are the most significant potential expansion of state financial control in human history, and they are being introduced in language so boring and technical that most people will not understand what they are agreeing to until it is operational.

Let me describe what a CBDC actually is in its full technical design. A central bank digital currency is money issued and controlled directly by a central bank — not mediated through commercial banks, not held in accounts with any institutional buffer between the citizen and the state. It is programmable money. Programmable means it can carry rules embedded in the currency itself.

What kinds of rules? The design specifications being developed by central banks around the world — and these are public documents, not speculation — include the ability to set expiration dates on currency. Money that expires if not spent by a certain date. The ability to restrict categories of purchase. Currency that cannot be used to buy certain goods or services, as determined by the issuing authority. The ability to apply negative interest rates directly to held balances — meaning the longer you hold the money, the less it is worth, as a mechanism to force spending. The ability to freeze balances or restrict access based on compliance with government requirements.

The Atlantic Council tracks CBDC development globally. As of early 2026, 134 countries representing 98% of global GDP are exploring CBDCs. Eleven countries have fully launched. China's digital yuan — the e-CNY — is already in use with 260 million wallets activated and documented tests of expiring currency and purchase category restrictions.

I want to be clear about what I am not saying. I am not saying that every government implementing a CBDC intends to use these capabilities oppressively. I am saying that these capabilities are being built into the architecture — and that capabilities that exist will eventually be used. History does not offer examples of surveillance and control infrastructure that governments built and then declined to use when circumstances made use convenient.

The financial identity you carry into a CBDC world is everything. If your financial access is contingent on compliance with whatever the issuing authority requires, you are not a citizen with rights — you are a participant on terms set by the state. The person who has a permanent, independently verified identity that cannot be revoked or restricted by a platform or government — that person has something the CBDC architecture cannot easily capture. That is what the Nexus Passport is designed to be.

NeuraWeb: Bitcoin was supposed to be the answer to all of this. Decentralized. Censorship resistant. Why did it fail the people it was supposed to help?

Vincent: Bitcoin did not fail as a technology. It failed as a solution to the problem it was positioned to solve — which was financial empowerment for the people most harmed by the existing system.

The whitepaper is elegant. A peer-to-peer electronic cash system. No central authority. Mathematically enforced scarcity. Transactions that cannot be censored or reversed. Every word of that is true. The problem is what happened in practice.

Bitcoin became an investment asset before it became a currency. The people who adopted it earliest — who had the technical sophistication to understand what it was in 2009, 2010, 2011 — were disproportionately already financially literate, already connected to technology, already in a position to hold a speculative asset and wait. The people who arrived in 2017 and 2021 — the retail waves — bought at peaks created by the early holders taking profit. The wealth transfer was from late adopters to early adopters. This is not fundamentally different from the system Bitcoin was supposed to replace.

The volatility problem is disqualifying for the use case that matters most. A person living paycheck to paycheck — which is 64% of Americans — cannot hold a currency that loses 70% of its value in a bear market. They cannot price goods and services in something that doubles and halves inside a calendar year. The people who most need an alternative to inflationary fiat currency are exactly the people least able to absorb the volatility of a speculative asset.

The identity problem was never solved. Bitcoin transactions are pseudonymous but not anonymous — every transaction is on a public ledger, permanently. What Bitcoin lacked was a way to connect a verified human identity to a wallet in a way that created trust without creating surveillance. Without that, Bitcoin could not become the basis of a real financial system. You cannot get a mortgage, run a payroll, or receive a government benefit through a system that has no verified identity layer.

And the environmental and complexity costs priced out the people who needed it most. Running a full node, understanding key management, avoiding the catastrophic errors that have resulted in billions of dollars of permanently lost Bitcoin — this is not accessible to the median person. The tools that were built on top of Bitcoin to make it accessible — exchanges, custodians, wallets — recreated exactly the intermediary infrastructure that Bitcoin was supposed to eliminate. And those intermediaries — FTX, Celsius, BlockFi — collapsed with customer funds in ways that recalled the worst of the banking crisis.

The problem was never the currency. The problem was the identity and the tools. Without a verified, permanent identity that you own — that cannot be taken from you, that travels with you across every financial interaction — you cannot build a fair financial system. You are always dependent on an intermediary who holds the identity on your behalf and can revoke your access at any time.

That is the gap NeuraWeb is filling. Not with a cryptocurrency. With a permanent verified identity and tools built on top of it that are priced for the people who need them, not for the people who are already fine.

NeuraWeb: So let's bring this together. What is NeuraWeb's structural answer to all of this — the Cantillon Effect, the petrodollar fracture, financialization, CBDCs, the failure of crypto?

Vincent: The answer starts with identity — and it has to, because everything else depends on it.

The reason the average person is financially vulnerable is not primarily that they lack information, though they do. It is not primarily that they lack tools, though they do. It is that they have no permanent, verified, portable financial identity that they own. Their financial life exists inside institutions that they do not control — banks that can close their account, platforms that can deplatform them, employers that can terminate access to their payroll system, landlords who can reject them based on a credit score produced by a private company using their data without their meaningful consent.

The Nexus Passport changes that architecture. One permanent identity. Verified. Heir-transferable. 150 years of persistence. No institution can revoke it. No platform can deplatform you from it. It is the foundation on which everything else we build sits — and it is the single most important financial tool we offer, even though most people initially think of it as just a login.

On top of that identity, SynergyLife provides the tools that financial advisors have always provided to people who could afford financial advisors. Budgeting. Net worth tracking. Real-time credit monitoring. Debt payoff optimization. AI-powered insights through Sally. One-click CPA access with a full audit trail. These are not novel inventions. They are existing capabilities, previously gated behind fees that made them inaccessible to the people who needed them most, made available at a price that reflects what they should cost in a world where we are not extracting rent from captive users.

NeuraPOS addresses the financialization of commerce directly. The 2.6% card processing fee is a tax on every transaction in the economy — paid by businesses, passed to consumers, collected by payment processors who contribute nothing to the transaction except the infrastructure they built once and have been extracting rent from ever since. At 0.5%, we are returning $2,100 a month to a business doing $100,000 in monthly card volume. At scale, across the NeuraWeb merchant ecosystem, that is a meaningful redistribution of economic value from extraction infrastructure back to the people doing actual commerce.

The transparency layer — the economic dashboard, the government spending data, the governance efficiency index — is the piece that I believe matters most in the long run, even though it generates no direct revenue. The Cantillon Effect operates invisibly. The petrodollar fracture is happening in documents that nobody reads. Financialization is so normalized that people blame themselves for not being able to afford a house rather than the mechanism that priced them out. CBDCs are being built in the language of bureaucratic modernization. When people can see these things — when the data is in front of them in plain language, updated in real time, with the context to understand what it means — the conditions for accountability change.

Governments protect advantage through opacity. Every meaningful reform in financial history came after people could see what was happening to them. Visibility is not sufficient. But it is necessary. And we are building the infrastructure that makes it possible.

NeuraWeb: Last question. The finances.nw page ends with "the only missing variable is whether enough people decide to use them." How many people need to decide before it matters?

Vincent: Enough to make the alternative real. I don't have a number. I know the direction.

Every person who processes a transaction through NeuraPOS instead of Square is $2,100 a year that doesn't go to a payment processor. Every person who uses SynergyLife instead of paying a financial advisor is access to tools that were previously gated. Every person who claims a Nexus Passport has an identity that they own — that no platform, no bank, no government can revoke without recourse.

The network effect of financial empowerment works in the opposite direction from the network effect of surveillance capitalism. Surveillance capitalism becomes more powerful the more data it accumulates — which means more people joining makes the extraction more efficient. Financial empowerment becomes more powerful the more people participate — which means more people joining makes the tools cheaper, the identity more trusted, and the alternatives more viable.

We are at 18,114 Founding Architects. The window is open. The tools are built. The data is real. The mechanism that has been extracting value from the average person for decades is documented and named on a public website that anyone can read for free, right now, at finances.nw.

The only missing variable is whether enough people decide to use what we built. I think they will. Not because I am an optimist — though I am — but because the alternative is to keep paying.

finances.nw is accessible now at neuraweb.io/finances.nw. Create your Nexus Passport free at neuraweb.io/une.nw. SynergyLife is free to start. SynergyOps begins at $99.99/mo.